Insurance customer engagement for complex claims workflows

ScaleLabs helps ops-heavy B2B teams ship client portals and workflow automation that reduce email chaos, speed up onboarding, and improve visibility across the business.

When a claim gets messy, multiple properties, injured parties, TPAs, outside counsel — the experience for your policyholder mostly comes down to how clearly you keep them in the loop. Insurance customer engagement becomes a lever not just for satisfaction, but for cycle times, leakage, and adjuster burnout.

As more parties join a claim, your “process” turns into overlapping email threads, shared drives, and spreadsheets. Everyone is working hard; no one can see the whole picture. This guide shows how insurers can replace that chaos with a single source of truth that works for policyholders, brokers, and internal teams.

Coordinated complex claims engagement starts with a shared, single source of truth for every stakeholder.

TL;DR

- Complex claims quickly overwhelm email- and spreadsheet-based processes.

- Policyholders want clear, proactive communication and simple digital touchpoints.

- A “single source of truth” is a shared claims workspace, not just a data warehouse.

- AI can route tasks, check documents, and trigger updates while humans handle judgment calls.

- ScaleLabs helps insurers build custom claims portals and workflows on top of existing systems.

able of contents

- Why complex claims break traditional customer engagement

- What good engagement looks like in claims

- How can insurers improve insurance customer engagement in complex claims?

- The problem with email-driven claims workflows

- What a single source of truth actually is

- Key building blocks across the claims lifecycle

- Where AI fits (and where it shouldn’t)

- Steps to move from chaos to coordination

- How ScaleLabs supports insurers

- Metrics to track as you modernize claims engagement

- FAQs from claims, ops, and IT leaders

- Bringing it together

Why complex claims break traditional customer engagement

Most carriers have done something digital in claims — web FNOL, a basic portal, maybe SMS status updates. That works for simple files but breaks on multi-party, multi-month claims with adjusters, engineers, vendors, and counsel.

At that point, customer engagement isn’t “send more updates.” It’s about orchestrating people and systems so the policyholder isn’t stitching the story together in their inbox.

“Complex claims fail not because people don’t care, but because the work lives in too many places for anyone to see it clearly.”

Industry research shows the same pattern: outcomes improve when communication is easy and journeys are coordinated. The J.D. Power 2025 U.S. Property Claims Satisfaction Study links higher satisfaction to easy communication and faster resolution, while Accenture’s omnichannel insurance client experiences overview calls for connected, AI-enabled journeys instead of fragmented, channel-specific experiences.

What good engagement looks like in claims

When policyholders describe a good complex claim, they usually say things like:

- “I always knew what was happening and why.”

- “I had one place to go for updates and documents.”

- “If I emailed or texted, someone responded quickly — and they already knew the context.”

From a system point of view, that means:

- A clear owner for each stage of the claim (triage, investigation, negotiation, settlement).

- Shared visibility for brokers, TPAs, and vendors, with role-based access to documents and notes.

- Communication channels (email, SMS, portal messages) that all feed into the same record.

In other words, good insurance engagement in claims is operational: every real-world step is logged, visible, and easy to explain to a stressed-out customer.

How can insurers improve insurance customer engagement in complex claims?

Improving insurance customer engagement in complex claims starts with making the work itself easier to follow. Policyholders do not want more messages; they want fewer surprises and one place where everything makes sense.

- Design around the customer journey. Map the real steps a claimant goes through and turn those into clear stages, owners, and milestones.

- Give everyone a shared workspace. Replace scattered threads with a single case view where policyholders, brokers, TPAs, and vendors can see status, documents, and next actions.

- Build proactive communication into the workflow. Trigger updates automatically when key events happen instead of relying on manual follow-ups.

- Use AI to keep the process moving. Let AI classify documents, flag missing information, and draft plain-language updates while humans handle judgment calls.

- Measure and iterate. Track satisfaction, cycle time, email volume, and workflow completion so you can see whether changes are actually improving the experience.

The problem with email-driven claims workflows

Email is great for quick questions, but it’s a weak backbone for a complex, regulated process that might last 6–18 months.

A typical email-driven claims workflow looks like this:

Email is useful for quick questions, but complex claims need a shared workspace that organizes every message and document.

- FNOL comes in via web form or call center.

- An adjuster starts emailing the policyholder, broker, and vendors.

- Attachments and key decisions end up scattered across inboxes and chat threads.

Aspect

Email-based workflow

Single source of truth workflow

Where work lives

Individual inboxes and shared drives

Shared case workspace linked to core systems

Customer view

Scattered threads and attachments

One portal with status, documents, and actions

Leadership view

Lagging reports, anecdotal updates

Real-time view across claims, teams, and bottlenecks

Claims leaders we work with at ScaleLabs describe the same pain: once a claim becomes complex, nobody can see whether delays sit with the carrier, the vendor, or the customer because that insight is buried in inboxes. Many operations teams solve this for suppliers with vendor portal software; complex claims need the same kind of shared, role-based workspace.

What a “single source of truth” actually is in claims

“Single source of truth” gets thrown around a lot. In claims, it’s less about one giant database and more about a shared front door for the work.

A practical way to think about it is the C.L.A.I.M. framework:

- Clear ownership — Every task has a single owner and due date.

- Logged steps — Every contact, document, and decision is attached to the claim.

- Automated nudges — The system prompts next steps instead of relying on memory.

- Integrated channels — Email, SMS, and portal messages all roll into one record.

- Measurable progress — You can see where files stall and why.

Technically, this might sit as a claims portal that talks to your core policy system, document management, and CRM. From the customer’s point of view, it’s just “the place I go to check on my claim and send what’s needed.”

Key building blocks across the claims lifecycle

To replace email chaos with a single source of truth, you don’t need to rebuild your claims organization; you need to spot where coordination breaks down and introduce shared workflows, one stage at a time. EY’s work with French insurer MACIF shows how a digital platform with an end‑to‑end view of customer requests and omnichannel routing can improve experience for both customers and employees; see EY’s digital platform customer experience case study for details.

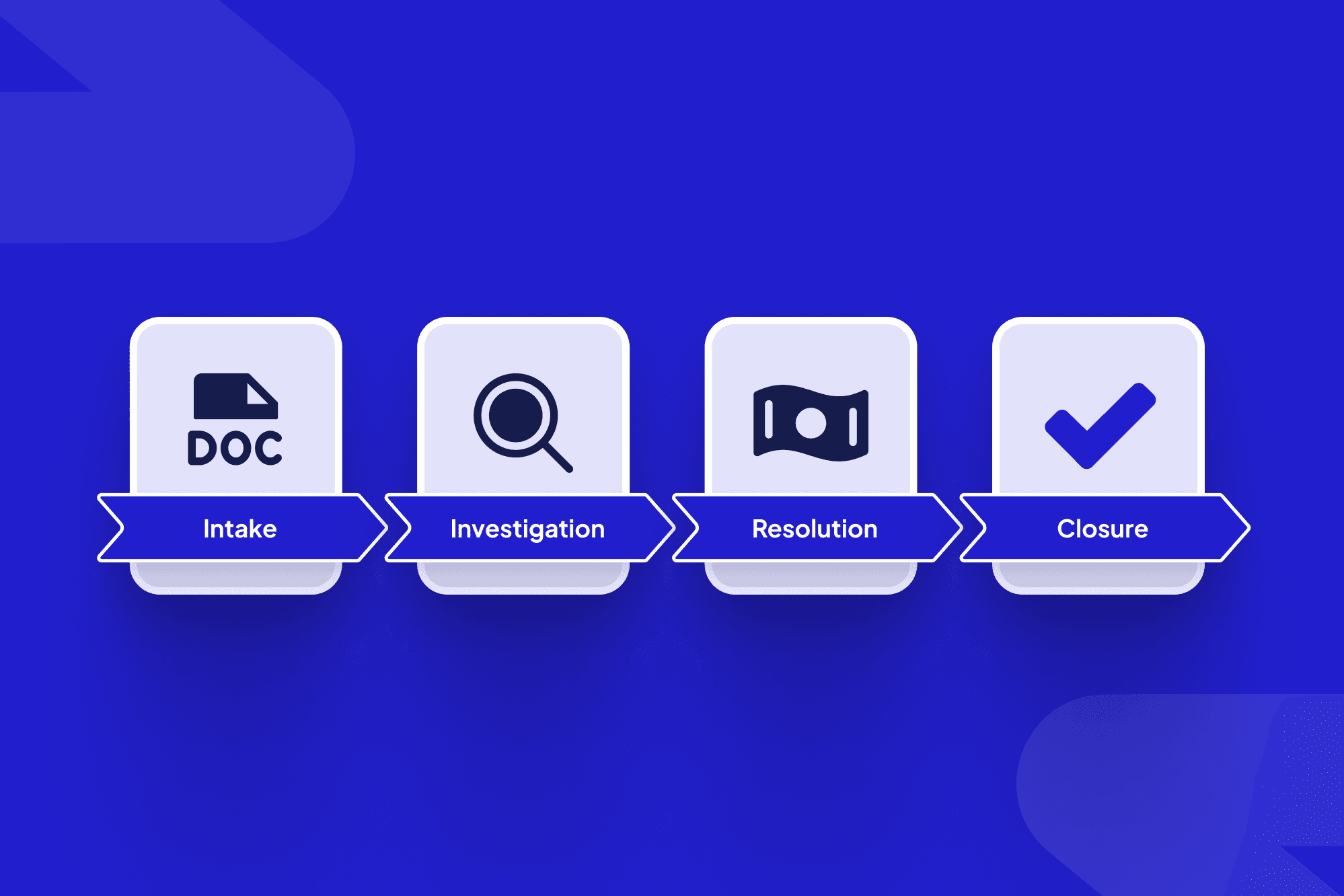

1. Intake & FNOL

FNOL data should flow into a central workspace that checks for missing information and routes the claim to the right team based on line of business, severity, and geography.

2. Triage & assignment

When an adjuster is assigned, they should see a single view with policy details, prior contacts, broker information, and uploaded evidence, and all outreach — email, SMS, or phone — should automatically log to the same claim record.

3. Investigation & documentation

Instead of sending attachments to an email address, policyholders and external experts use a secure link to upload documents, sign forms, and answer structured questions, with role-based permissions controlling who sees what. If you have digital vendor onboarding workflows elsewhere in your business, the goal is similar: one predictable, auditable flow instead of ad hoc email requests.

4. Negotiation, settlement, and payment

Draft settlement letters, approvals, and payment steps move through the workflow with clear SLAs, and policyholders can see what’s pending, what’s approved, and what’s in payment processing, reducing the “just checking in” messages that eat up adjuster time.

5. Recovery, subrogation, and closure

For claims that involve recovery or subrogation, the same workspace ties together internal counsel, external firms, and third parties so that, at closure, the full story is available for audit, analytics, and underwriting feedback loops.

Where AI fits (and where it shouldn’t)

AI shows its best side in claims when it handles “directional” work: classifying, checking, routing, and summarizing so humans can focus on judgment.

AI works best when it supports adjusters with triage, routing, and summaries, while humans stay accountable for coverage and settlement decisions.

Examples insurers are already seeing value from:

- Classifying incoming emails and documents and attaching them to the right claim.

- Detecting missing information based on policy type and coverage.

- Summarizing long claim histories into a single page for new handlers.

- Drafting plain-language status updates for adjusters to review and send.

Industry analyses suggest that carefully deployed AI can increase productivity in insurance processes and reduce operating expenses, especially in claims and servicing; for a high-level view across the value chain, see this AI in insurance overview.

What AI shouldn’t do is make unchecked coverage decisions or settle claims on its own. At ScaleLabs, our AI workflow automation platform handles triage and communication support while humans sign off on the moments that matter for risk, compliance, and customer trust.

Steps to move from chaos to coordinated claims engagement

You don’t need a multi-year transformation program to get started. Most carriers begin with one line of business, geography, or severity band where email chains are already painful and treat that as a focused pilot.

- Pick a painful slice of claims. Choose the segment where email chains are longest and handoffs are most confusing, and make that your pilot area.

- Map the real workflow. Treat this like a quick workflow analysis: whiteboard how work actually moves today across adjusters, brokers, TPAs, and vendors.

- Identify touchpoints for a shared workspace. Mark the points where a portal or shared case view would reduce back-and-forth and clarify ownership.

- Connect to your existing stack. Start by integrating with core policy admin, claims, and document systems so data stays consistent without replacing systems of record.

- Layer in AI assistants gradually. Begin with low-risk tasks such as classification, summarization, and drafting, then expand once controls and governance are proven.

External research from McKinsey and Deloitte shows that carriers who digitize end-to-end claims journeys and modernize operating models can raise satisfaction while lowering claim costs. McKinsey’s next-generation operating model article and Deloitte’s view on the future of insurance claims management both emphasize using automation, analytics, and straight-through processing to remove friction at each handoff.

How ScaleLabs supports insurers

ScaleLabs works with operations-heavy insurers to design and build custom claims portals and internal workspaces that sit around your existing core systems, giving policyholders, brokers, and teams a shared, AI-assisted workflow instead of scattered email chains.

In one engagement with an engineering firm, a centralized, AI-enabled project portal—similar to the approach in our guide to AI automation in engineering projects—moved more than 80% of client communication out of email within 90 days and cut manual admin time by about half. Coordinators went from juggling five disconnected tools to working from a single workspace where every request, file, and status lived in one place.

If you’d like to explore a pilot for one of your complex-claims segments, you can book a call, and we’ll map a real workflow with your team and outline a pragmatic, production-ready solution.

Metrics to track as you modernize claims engagement

To know whether your new workflows are working, you’ll want a simple scorecard that speaks to operations, customer experience, and finance.

A simple claims metrics dashboard helps leaders track customer experience, cycle times, and workflow adoption as engagement improves.

- Policyholder experience: NPS or CSAT for claims, complaint volume, and escalation rates.

- Speed & reliability: Cycle time from FNOL to settlement and the average time between key status updates.

- Communication load: Emails and calls per claim, first-response times, and handoff delays.

- Workflow & adoption: Percentage of claims that follow the designed workflow and how often adjusters, brokers, and vendors use the shared workspace instead of email.

- Operational efficiency: Claims handled per FTE, overtime patterns, and rework caused by missing or incorrect data.

If you already track adoption and cycle times for other portal initiatives, such as vendor or partner onboarding or your procure to pay automation, you can reuse much of that thinking here. Our guide to B2B partner onboarding walks through similar metrics for turning email-heavy approval flows into predictable, portal-driven workflows.

FAQs from claims, ops, and IT leaders

“Is this just another portal project?”

Not if it’s done right. The goal is a shared workflow that ties together your core systems, documents, and communication channels; the portal is simply how people access it.

“Will this replace our core claims platform?”

No. In most cases, the engagement layer integrates with your core claims platform via APIs or secure integrations and doesn’t attempt to replace the system of record.

“How do we handle security and compliance?”

Solutions typically include SSO/SAML integration, magic link authentication for simple, secure access, role-based access controls, encryption at rest and in transit, and detailed audit logs so compliance teams can see who did what and when.

“What’s a reasonable first step?”

Many insurers start with a short discovery engagement to map a specific claims workflow, surface the biggest engagement gaps, and define a pragmatic pilot before expanding.

Conclusion

Bringing it together: email where it helps, workflows where it counts

Email isn’t going away; policyholders will keep replying from their inbox and brokers will keep forwarding something at 4:59 p.m. The difference is whether those messages land in personal inboxes or in a shared, AI-assisted workflow that keeps everyone on the same page.

For carriers, better claims engagement isn’t just a nicer experience. It’s a way to shorten cycle times, lower leakage, and give your teams a calmer, clearer way to run complex work.

Key takeaway

Treat complex claims engagement as an operations problem, not just a communication problem. Build a single source of truth around your existing stack, and use AI to keep the work moving — with humans firmly in charge of decisions.

This article was created with the assistance of AI and reviewed by the ScaleLabs team for accuracy and relevance.